Customs update: EU-Mercosur agreement enters Into force

As of May 1st, the new EU-Mercosur Agreement (covering Brazil, Argentina, Paraguay, and Uruguay) is officially in effect. This agreement brings significant, phased tariff reductions for European importers of products like limes, melons, and grapes. But it also introduces strict new customs requirements.

What you need to know:

Lower import duties: Tariffs on frequently handled agricultural products like limes, melons, and grapes are dropping immediately as part of a 15-year elimination plan.

Strict paperwork rules: To actually benefit from these lower rates, your South American suppliers must be officially registered in their home country and include a valid 'Statement on Origin' directly on the commercial invoice.

Get it right the first time: This correct documentation must be in place before customs clearance. Without it, the standard higher tariffs will apply. While claiming the discount retroactively is possible, it requires filing an incomplete declaration, which will cause delays and extra handling fees.

If you are importing from these regions, ensure your suppliers are aligned with these new rules immediately to protect your margins and prevent bottlenecks.

Straight of Hormuz

Please note: The geopolitical situation in the Middle East is very dynamic. The information below reflects the current status, but the news is developing quickly and the situation on the water may shift again in the coming days.

Monthly fuel surcharges & slow-steaming

The ongoing closure of the Strait of Hormuz is causing swings in global bunker prices. To cope with these rising costs, ocean carriers are changing how they calculate fuel surcharges and operate their vessels.

Here you can find the current Emergency Bunker Surcharges for import from Asia.

What is changing in the market:

Monthly fuel surcharges: Instead of adjusting bunker formulas every three to four months, carriers are switching to a monthly rhythm for Emergency Fuel Surcharges (EFS). This allows them to recover their expanding costs faster.

Inland costs affected: These emergency surcharges are no longer limited to just the ocean leg. Carriers are now extending them to cover higher fuel costs for third-party feeders, intermodal rail, and cross-border trucking. This adds complexity and makes your total landed costs much harder to predict.

The return of slow-steaming: To mitigate the fuel prices, carriers are actively reducing vessel speeds to save fuel. The average speed of container ships has dropped to its lowest point since March 2023. Analysts warn that even if the Strait reopens, vessel speeds will likely take a long time to recover.

What can you expect: Prepare for increased cost volatility in the short term. With fuel surcharges now being updated monthly and extending into your pre- and on-carriage, predictability is reduced. Additionally, be sure to factor the return of slow-steaming into your inventory planning, as ocean transit times might be longer. (The Loadstar)

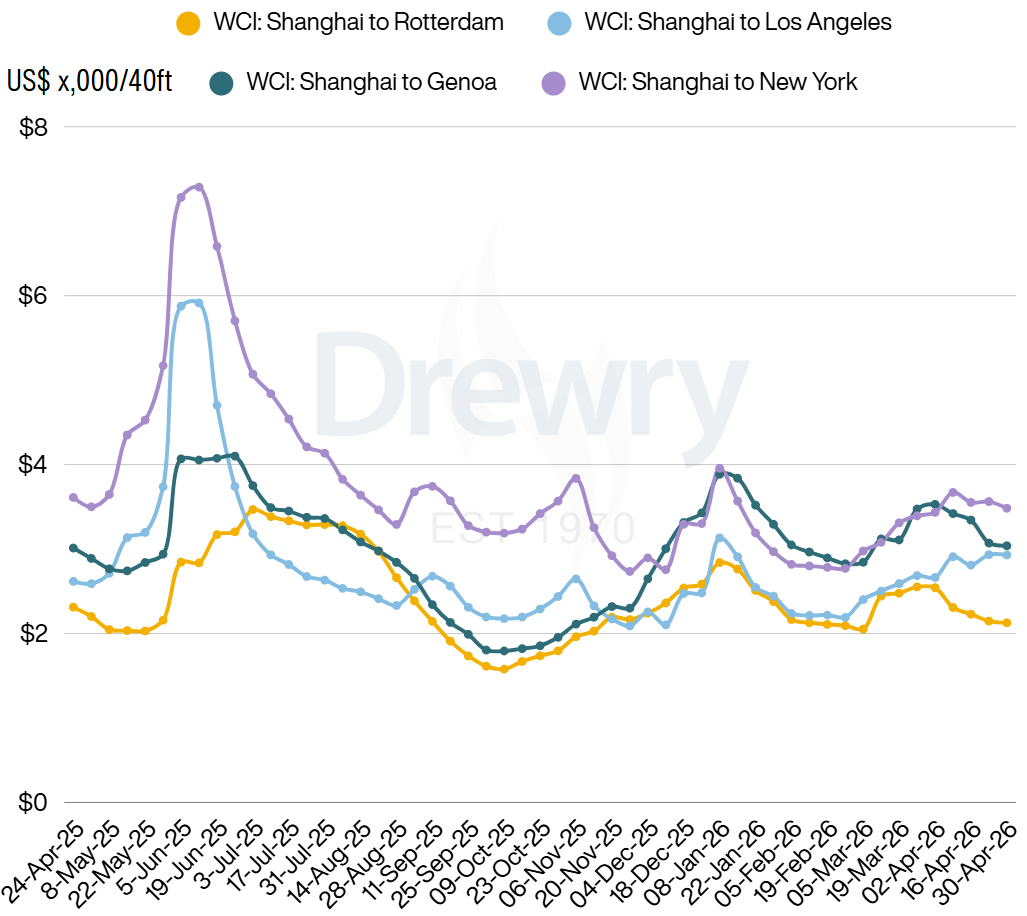

Ocean rates: Asia-Europe rates declines as carriers prepare for May

While the Asia-US rates are going up, container spot rates on the Asia-Europe trade have their third consecutive week of declines. However, carriers are actively stepping in to reverse this downward trend.

What is happening in the market:

Asia-Europe rates soften: Spot rates from Shanghai to Northern Europe and the Mediterranean have continued their slow decline, dropping another 1% this week. Market data shows that rates on this lane peaked about three weeks ago.

Carriers slash capacity: We see that carriers are trying to reduce capacity with blanc sailings and to keep the rates on higher levels. Not only blanc sailings, but also using smaller vessels to reduce capacity. At the end of April we have seen a mini Peakseason because of the "Golden Week" Holiday.

Looking ahead: For the second half of May carriers want to implement the higher FAK rates to support them. Looking at the market demand it will be difficult to maintain this.

The Asia-US exception: In contrast to Europe, rates from Asia to the US West Coast are actually rising. This is largely driven by US shippers adopting a "better safe than sorry" approach. They are front-loading their inventory now to avoid potential bottlenecks and congestion during the traditional Q3 peak season.

While most carriers continue to avoid the Red Sea, CMA CGM is increasing its Suez Canal transits for specific routes to fourteen 7.000 - 10.000 TEU ships . Driven by high bunker costs and shippers willing to pay a premium for faster transit, the French carrier is resuming the shorter route for selected services.

What is changing:

Faster Asia-Europe transit: The new Asia-Europe (OCR) service is routing through the Suez Canal. This direct connection saves approximately two weeks on a round-trip rotation compared to the longer Cape of Good Hope detour.

Split routing for India: The India-Europe (EPIC) service will route its westbound (to Europe) vessels through the Suez Canal, while eastbound (from Europe) sailings will continue to take the Cape route. Note that calls at Abu Dhabi, Jebel Ali, and Sohar have been temporarily dropped due to the Strait of Hormuz closure.

Potential market shift: CMA CGM's operational cost savings (needing fewer ships for a shorter round-trip) and the premium rates for Red Sea cargo could tempt rival carriers to follow. This could potentially set the stage for a fresh rate update if more capacity returns to the Suez. (The Loadstar)

New truck toll confirmed for July 1st

The Dutch government has confirmed that the new national truck toll (vrachtwagenheffing) will officially take effect on July 1st. While recent political debates sparked rumors of a delay until 2027, industry associations have clarified that the start date remains. However, the financial impact is currently under review. (Nieuwsblad Transport)

What is happening:

No delay, but potential rate cuts: The toll will go live on July 1st. However, due to the severe financial pressure on the transport sector (driven by high diesel prices and wages), the government is actively looking to lower the initially planned rates, which were set to reach up to 20 cents per kilometer.

Carriers in the starting blocks: Transport companies are ready to implement the new system but are currently waiting for the final, officially lowered rates to be published before they finalize new pricing agreements with their customers.

Gridlock for e-trucks: While electric trucks are subject to a much lower toll rate, carriers are struggling to transition. The Dutch power grid is currently highly congested, preventing many transport hubs from securing the electrical connections needed to charge a new e-truck fleet.

What can you expect: Even with potential rate reductions from the government, the adjustment of this toll will increase your inland transport costs in the Netherlands starting Q3. Expect your road freight partners to reach out in the coming weeks to finalize updated rate agreements as soon as the Dutch government publishes the definitive toll figures. (Nieuwsblad Transport)

Blank sailings: 6% cancellation rate

From 4 May to 7 June, 6% of sailings have been withdrawn (43 of 689 sailings).

The market is showing early signs of stabilisation. While carriers continue to adjust capacity and reroute cargo, the system is proving resilient.

Cargo throughput in the Port of Rotterdam remained stable in the first quarter of 2026, showing only a slight decrease of 0.7% (totaling 103.0 million tonnes). Despite the severe geopolitical tensions surrounding the Strait of Hormuz, the port continues to show resilience as a crucial European energy and logistics hub. (Flows)