Welcome back.

Importers of veterinary goods (such as meat and fish) are currently facing significant delays at the Port of Rotterdam. A recent inventory shows that at least 600 containers have been waiting for inspection by the NVWA for over a week.

Why is this happening?

A combination of factors is currently straining capacity:

Impact

Unfortunately, these delays are leading to increased demurrage and detention costs. To relieve the pressure, capacity has been scaled up: major inspection points are now performing inspections during evenings and weekends. While this adds capacity, the backlog has not yet been fully cleared. (Nieuwsblad Transport)

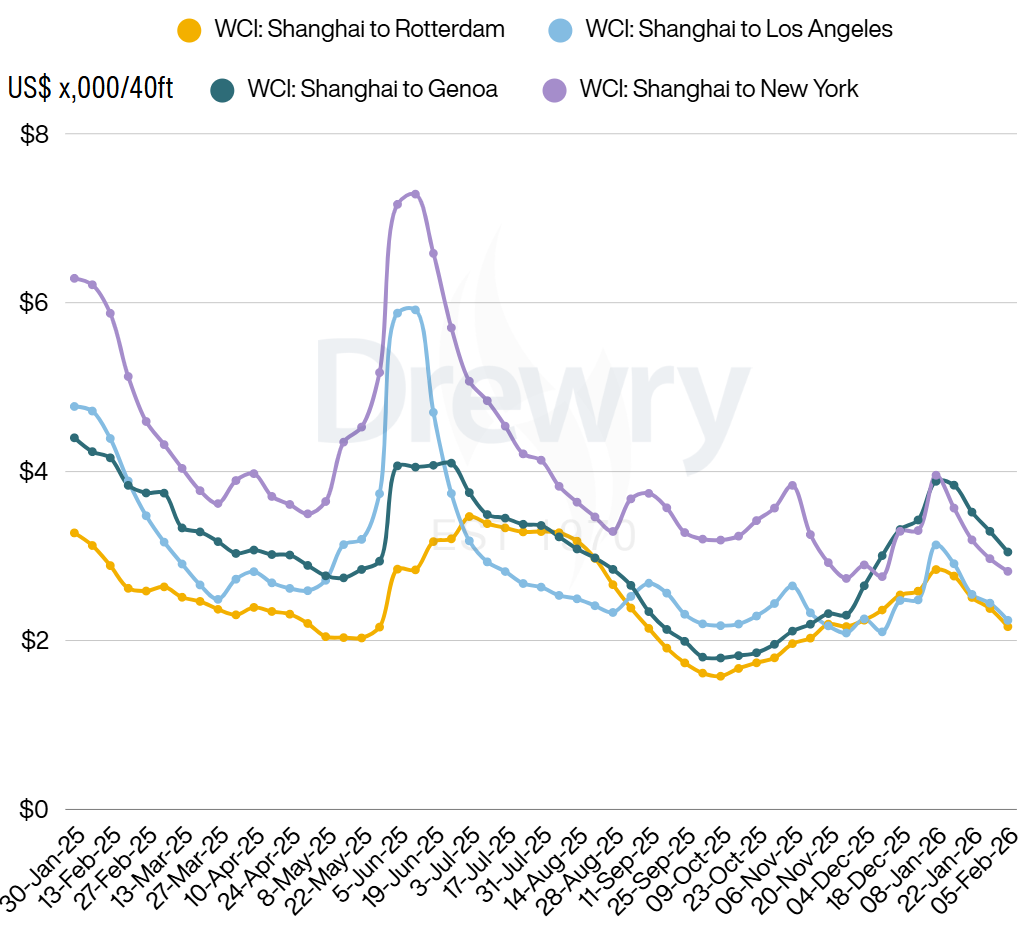

Spot rates on the Asia-North Europe trade decreased again this week. While the year started with a strong peak, the pre-Chinese New Year rush has faded, and rate levels are significantly lower compared to the same period last year.

A buyer's market

With demand cooling down, analysts predict that the downward trend will continue in the coming weeks until March. The market is shifting further in favor of shippers. To counter this, carriers are likely to blank more sailings (cancel trips) to maintain load factors during the upcoming quiet period. The first carriers are also announcing higher rates for March but this is not for sure yet.

Tensions are rising again at the ECT terminals in Rotterdam. Transport companies and drivers are dissatisfied with persistent waiting times and are actively considering new actions/strikes.

The core issue

Despite talks in January, waiting times have increased again, reversing earlier progress.

The outlook

ECT is working on long-term fixes, including hiring more staff, installing extra cranes, and modifying access routes. However, these measures have not yet reduced current waiting times, meaning the risk of operational disruptions remains high in the short term. (Nieuwsblad Transport)

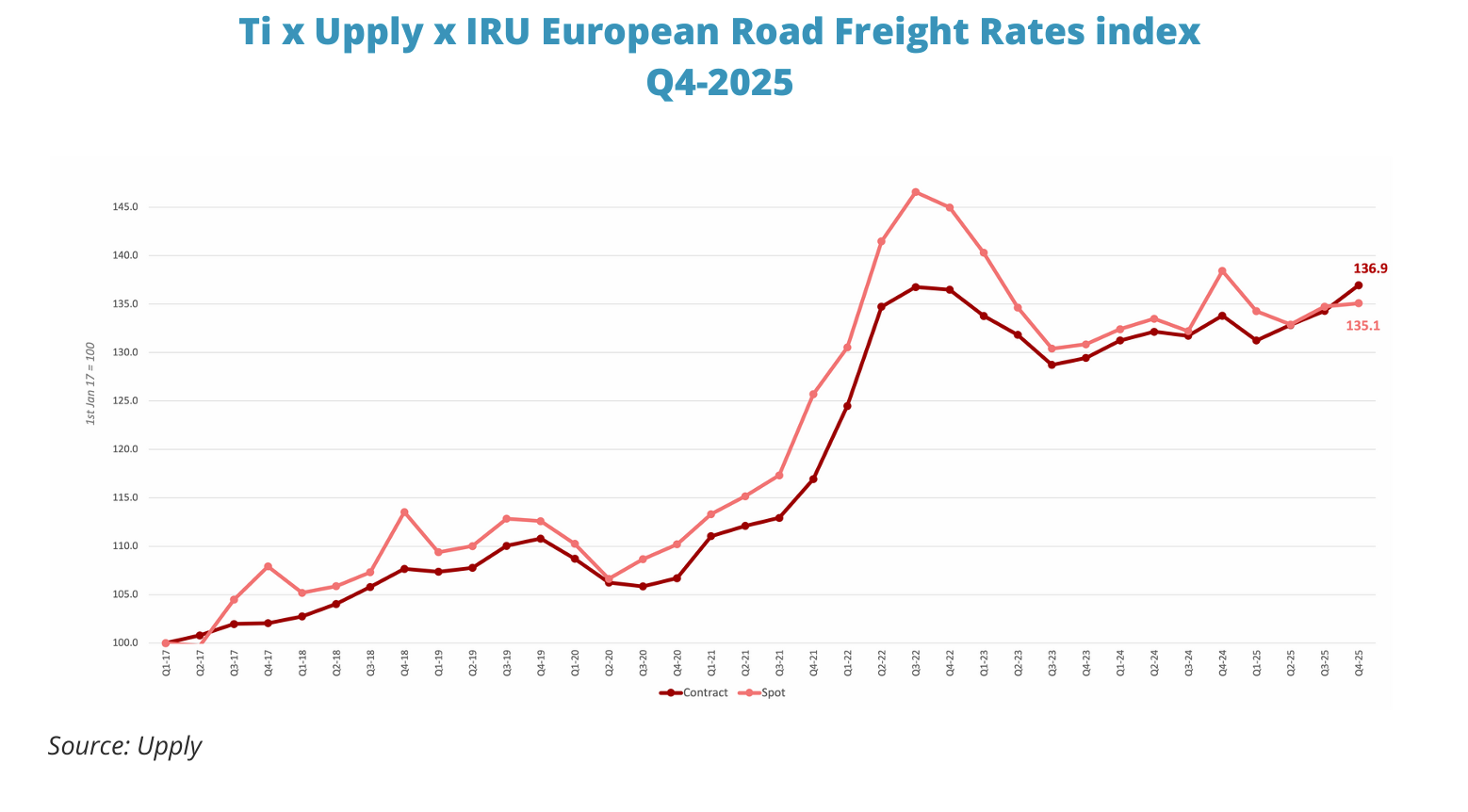

For the first time since 2017, long-term contract rates for European road freight have surpassed spot market rates. Contract rates climbed significantly in Q4, overtaking the spot market. This is driven by businesses locking in prices early to secure capacity for expected demand.

Cost drivers

Carriers are passing on rising operational costs, including increases in fuel (+0.7%), driver wages (+1.3%), and insurance (+4.2%).

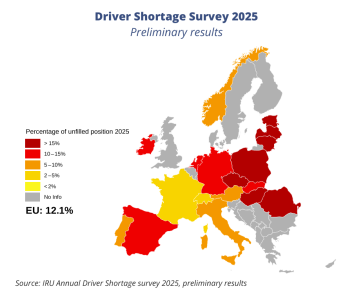

The bottleneck

While modest volume growth is expected for 2026, the industry faces a critical challenge: the driver shortage in the EU has risen to 444,000 unfilled positions. This scarcity, particularly in Germany and Eastern Europe, will likely keep pressure on rates and capacity throughout the year.

Suez canal: Gemini alliance attempts a return 🚢

Adding to the market dynamics is the potential return to the Suez Canal. In a significant operational shift, Gemini partners Maersk and Hapag-Lloyd have confirmed they will resume Suez Canal transits for their India-Mediterranean service starting mid-February.

The impact: This service utilizes high-capacity vessels and will release significant capacity back into the global fleet.

Why now? The carriers state that the route is currently safe enough, having secured naval protection for their vessels. Additionally, insurance premiums for the route have dropped significantly (from 1% to ~0.2-0.3%), making the transit commercially viable again.

The plan

Market context

This move marks a U-turn for Hapag-Lloyd, which previously ruled out a return. It stands in contrast to CMA CGM, which recently cancelled its own plans to resume Suez transits. Experts suggest that unless the security situation deteriorates, this could signal the beginning of a gradual return for the wider industry. (Nieuwsblad Transport)

The air cargo market is currently at a peak, driven by a perfect storm of seasonal events: the pre-Chinese New Year rush and the demand for Valentine’s Day perishables (flowers). We are seeing a "mini-peak" with rates increasing globally. Lanes from Taiwan, Southeast Asia, and China to both the US and Europe are showing particularly strong gains as shippers rush to move goods before the holiday shutdowns.

Interestingly, available capacity is rebounding and up significantly compared to last year. Airlines are injecting space into the market to accommodate flower shipments from Africa and Latin America. While rates are currently climbing, this recovery may be short-lived. With capacity growing faster than demand, the market is expected to soften again once the seasonal rush subsides after mid-February. (The Loadstar)