Welcome back.

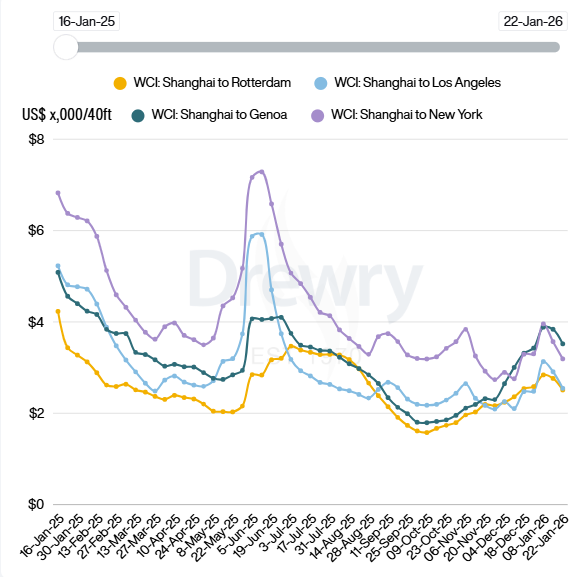

The pre-Chinese New Year season has taken an unexpected turn. Instead of the traditional rate surge and space crunch we usually see in late January, we are witnessing a significant drop in spot rates across all major trade lanes.

Recent data confirms double-digit declines on both Asia-Europe and Asia-America routes this week. Simply put, the demand is not keeping up with the available capacity. The early January "mini-rush" has ended quickly, and rates are going down much faster than anticipated. (Nieuwsblad Transport)

For importers, this is excellent news. Operationally, the network is currently very fluid. Vessels have enough space, and unlike the chaos often seen before the holidays, trucking operations in China are running remarkably smoothly. (The Loadstar)

European supply chains are facing a double challenge this week, with disruptions hitting both inland and at sea.

Belgian rail strikes

A major rail strike in Belgium started on Sunday, January 25th and is set to run through Saturday, January 31st. This comes at a difficult time, as ports like Antwerp and Rotterdam are already battling high yard utilization and congestion. With rail services heavily impacted, cargo is rapidly shifting to road transport. Expect tighter trucking capacity and potential delays on cross-border corridors as the road network absorbs the extra volume. (The Loadstar)

Vessel delays due to weather around the coast of France

Simultaneously, severe weather in the Bay of Biscay is forcing vessels to hit the brakes. Many ships destined for North Europe have interrupted their voyages to seek shelter off the coasts of the UK and France. Consequently, we expect arrival delays at all major North European ports in the coming days. (Nieuwsblad Transport)

Airlines are facing new operational hurdles this week as safety warnings regarding Iranian airspace force rerouting on Asia-Europe services. To avoid the conflict zone, carriers are diverting flights via Central Asia or the Arabian Peninsula, adding approximately 10-30 minutes to flight times and increasing fuel consumption.

Surprisingly, these rising operational costs are not driving up rates for shippers.

Despite the geopolitical longer routings, the market remains favorable. With enough space and lower rates, the pressure is currently off as we wait for the pre-Chinese New Year rush to materialize. (The Loadstar)

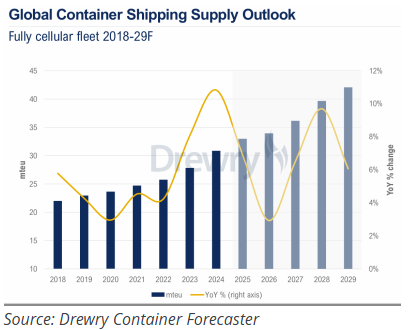

After years of rapid expansion, 2026 offers a brief moment of calm. Global fleet growth is projected to slow to around 3% this year, closely matching the expected demand. This dip is largely the result of a lull in ship orders back in 2023.

However, analysts warn that this balance is short-lived. A massive wave of new capacity is already in the pipeline for 2027-2029, driven by an aggressive "arms race" among top carriers like MSC, which has now secured 21% of the market share.

To keep the market balanced, older ships need to be retired. However, because these vessels are still earning good money, owners are in no rush to scrap them. This keeps extra capacity available, which will be a key driver for freight rates throughout the year.(The Loadstar)

Our latest data shows that the congestion of 2025 wasn't a fluke. It’s the new normal.

CMA CGM leads rethink on Suez return as political uncertainty rises