Welcome back.

Asia-Europe rates continue to rise, with Shanghai-Rotterdam up 3% and Shanghai-Genoa up 4%. Carriers are managing capacity tightly as 2026 contract negotiations begin, but weak demand may limit how long higher rates can hold. If these planned increases hold, Asia–Europe spot rates could rise sharply within weeks. European importers should be prepared for further upward pressure on short-term pricing and potential knock-on effects on contract negotiations for 2025. (The Loadstar)

In contrast, Spot rates on Asia-US trades saw a brief increase after the 1 November General Rate Increases (GRIs), but gains were quickly offset by carrier discounts. (The Loadstar) Rates then fell again, with Shanghai-Los Angeles down 12% and Shanghai-New York down 15%, showing soft underlying demand.

Road freight rates in Europe have also risen slightly compared to Q3 2024. Contract rates increased by 1.4% year-on-year, while spot rates went up 2.4%. This is partly driven by seasonal holiday demand, but also by a gradually improving economic outlook.

Analysts note early signs of recovery: manufacturing is stabilizing and consumer demand remains solid. However, the recovery is uneven across Europe: Germany continues to face headwinds, while Spain is showing stronger momentum.

Overall, the outlook is cautiously positive, but full market stability has not yet been reached. (Nieuwsblad Transport)

Last week, MSC sent an Ultra Large Container Vessel (ULCV) through the canal for the first time since the Red Sea crisis began. This is a sign that some carriers are cautiously testing the route again.

At the same time, the Middle East has become more stable, and some carriers have reopened services from the Middle East to the Mediterranean.

However, for Asia - Europe, the risk remains higher. Many vessels originally scheduled for the Red Sea are still diverting last-minute via the Cape of Good Hope. Bookings through the Red Sea remain limited, and any transit still carries operational risk. In short: the route is becoming more viable, but full-scale return isn’t guaranteed and not risk-free.

If carriers switch back to Suez quickly, ships currently spread along the Cape route could arrive in Europe at the same time as vessels already scheduled via Suez.This overlap could create major port congestion, similar to 2021 with the Ever Given. Up to 1,000 port calls may be affected in the first month, causing delays, empty container shortages, and temporary spikes in spot freight rates. (The Loadstar)

Because ULCVs can carry 10,000+ containers, even a few overlapping arrivals can overwhelm terminals. Carriers will need to coordinate closely to avoid several vessels hitting the same ports at once. In short: a rapid return to Suez could trigger heavy port congestion and short-term rate increases.

A large-scale return to Suez is unlikely in the very near future. Most carriers indicate they need stability before rerouting, and a gradual return is expected no earlier than after Chinese New Year. In the meantime, booking possibilities for Red Sea transits will stay limited, and shippers should prepare for schedule changes, and continued reliance on the Cape route.

Once the shift happens, we may see a brief surge in spot rates and longer transit times due to congestion. After this period, capacity will likely increase again, pushing rates down.Carriers are expected to respond with strategies like slow steaming, blank sailings, and vessel lay-ups.

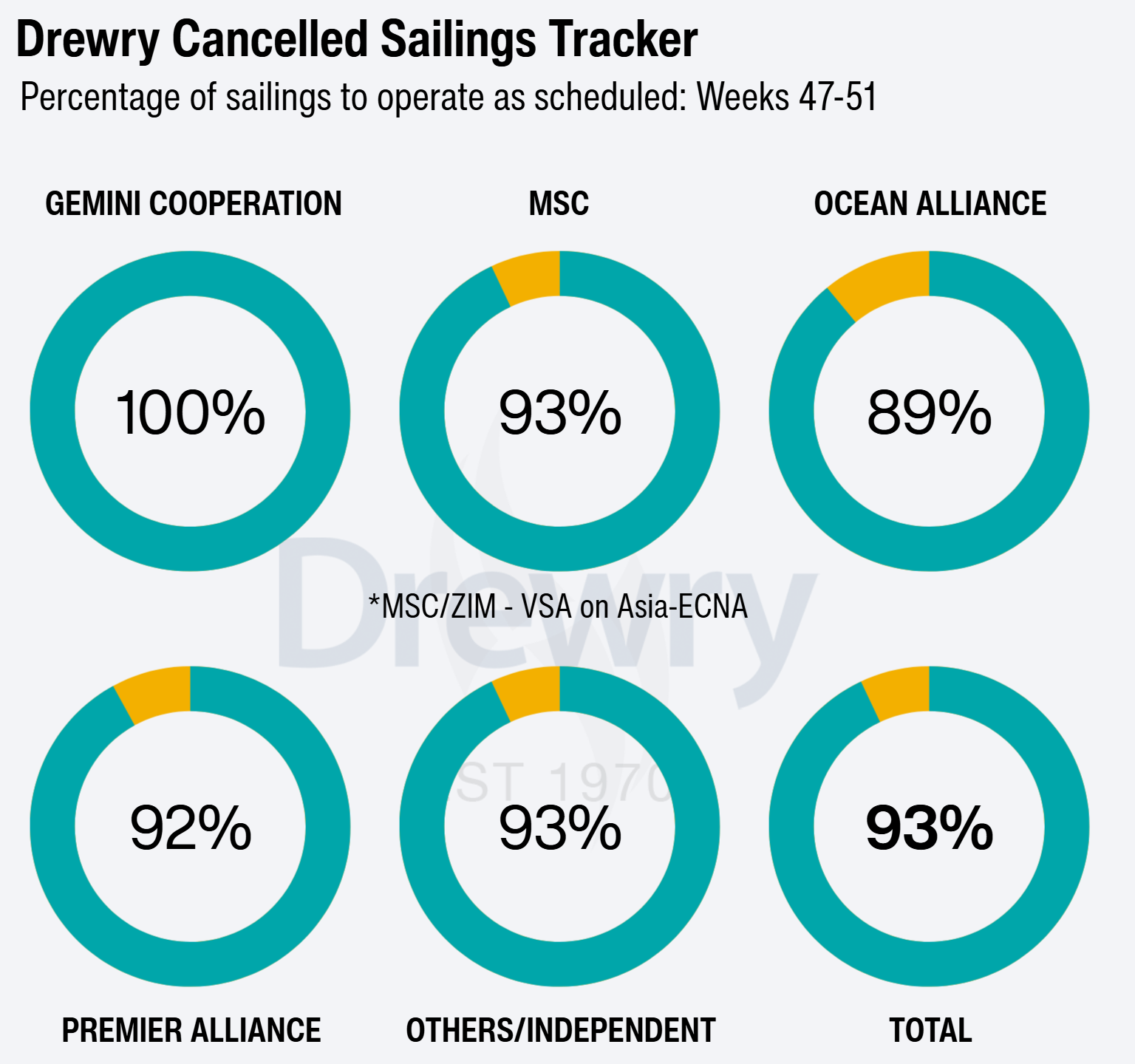

Hapag-Lloyd and Maersk are considering introducing a surcharge for shipments, arguing that the higher schedule reliability delivered through the new network justifies a higher price. Both CEOs recently confirmed that a premium is being evaluated, noting that the >90% on-time performance promised at launch provides shippers with significant logistical and cost advantages.

While early performance exceeded 90% reliability, Sea-Intelligence data shows on-time performance dipped slightly in August-September to 89.1% for all arrivals and 86.4% for western arrivals. Despite this decline, Gemini continues to outperform the industry average of 65.2%, although MSC is now approaching similar reliability levels. (Nieuwsblad Transport)