The market is under more pressure than at any point since the Red Sea crisis and it's coming from several directions at the same time.

The result: too much demand, not enough space, and rising costs: a perfect storm that is now being passed on to shippers through surcharges and higher rates.

Book as early as possible. Space is the scarce commodity right now. When it's available, it won't stay that way for long.

If you have shipments without strict delivery deadlines, please always consult with your Shypple contact person. Given the ongoing market pressure and the approaching traditional peak season in autumn, we prefer to look at strategic planning or alternative routings together, rather than simply delaying shipments.

Across major East–West routes, 47 blank sailings are expected over the next five weeks (week 23 to week 27 — June 1 to July 5), out of 707 scheduled departures. That is a 7% cancellation rate, with 93% of services still expected to sail as planned.

Where the cuts are concentrated:

💡 What this means for your shipments

Fewer sailings means fewer options. If your preferred departure is cancelled or full, the next available vessel may be a week later — and more expensive. The earlier you book, the more options you have.

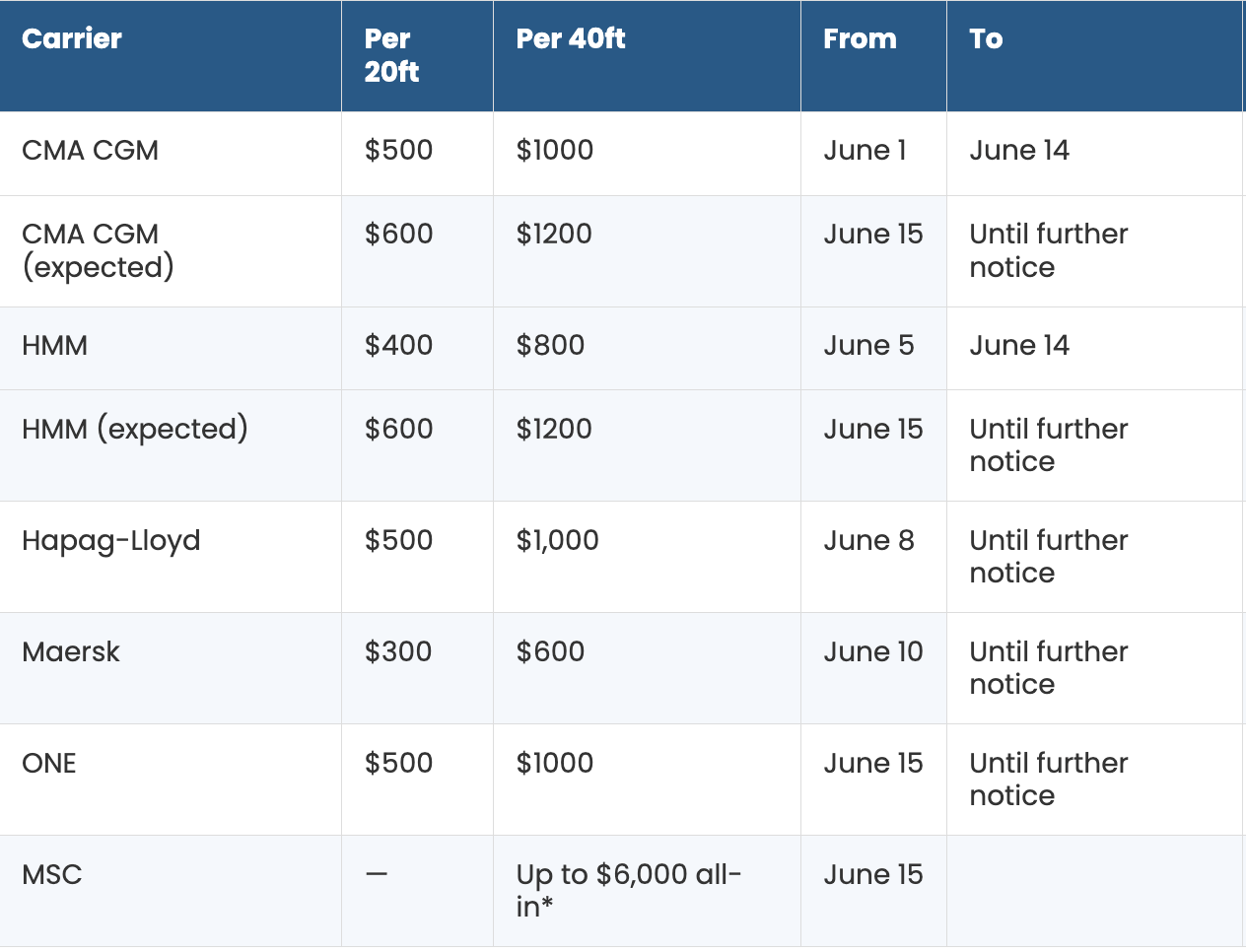

All major shipping lines have announced a Peak Season Surcharge (PSS) for June. This is a temporary fee added on top of your regular freight rate, for all container types from Asia to Europe and Mediterranean routes.

Please note: Unlike other carriers applying a temporary surcharge (PSS) on top of existing contract rates , MSC is implementing a General Rate Increase (GRI) targeting a new 'all-in' rate of up to $6,000 per 40ft container from Asia to North Europe, roughly doubling the current spot rate.

The word 'surcharge' is used for several different fuel-related costs. Here is the difference:

PSS — peak season surcharge

- A temporary add-on that carriers charge during busy periods. Announced with short notice.-

- Announced per sailing or per month. Here’s the overview, updates ongoing.

BAF — bunker adjustment factor

- The standard fuel surcharge in your contract. Covers normal fuel cost swings.

- Usually updated quarterly. July 1 update expected to be significantly higher.

EFS / EBS — emergency fuel/bunker surcharge

- An extra fuel surcharge on top of BAF, used when fuel prices spike unusually fast.

- Updated weekly or monthly for both general cargo and reefer. Currently active on most import lanes from Asia.

Fuel surcharges (local)

- Ongoing fuel surcharges for Dutch and Belgian trucking

- Updated weekly in this fuel surcharge overview.

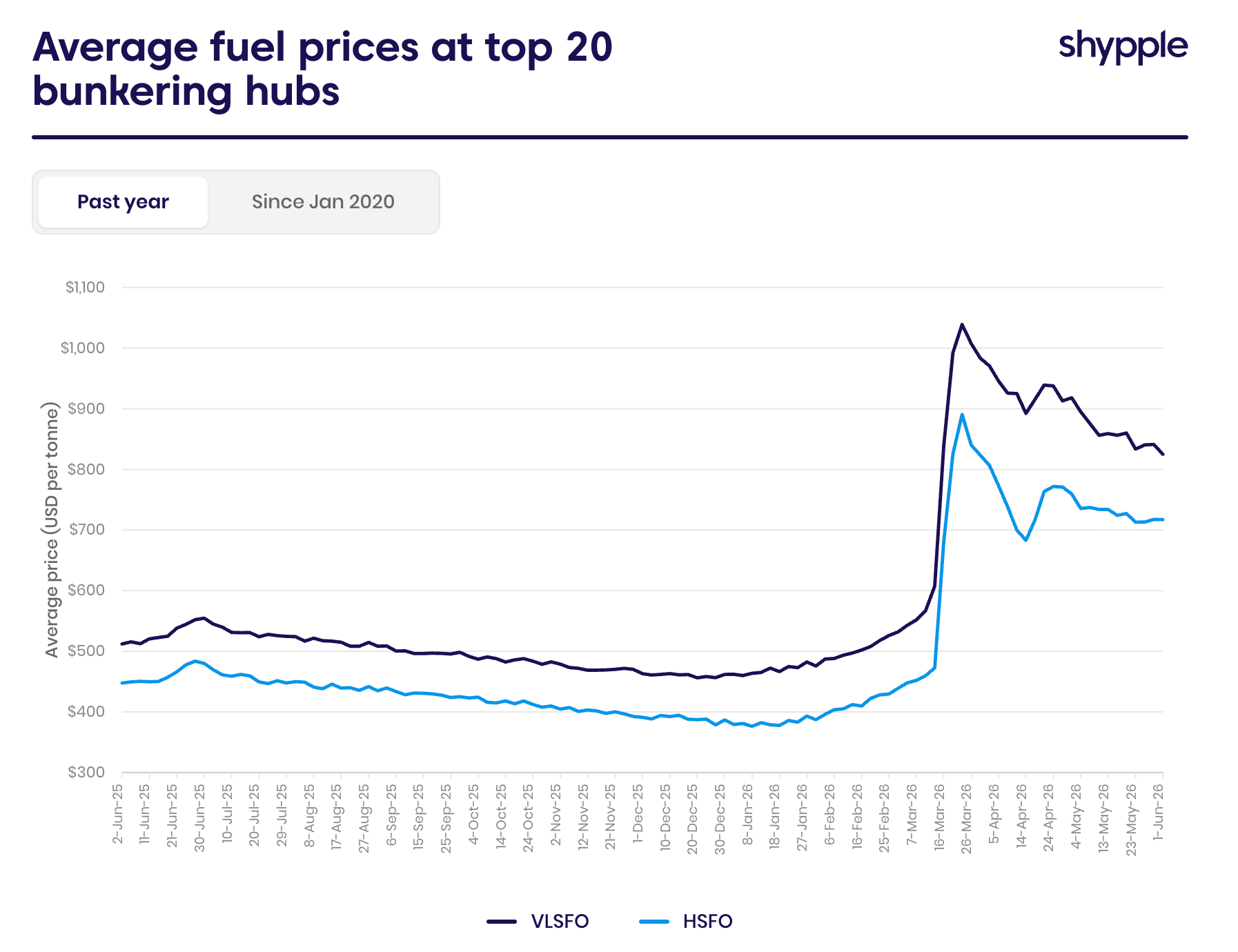

Bunker fuel costs for vessels are now 68% higher than in February. This is driven by escalations around the Strait of Hormuz — a vital transit point for roughly 20% of the world's oil supply. While this is a different geographical region than the Red Sea, the restricted oil flow drives up global energy prices, which carriers pass on directly through fuel surcharges.

Carriers update their standard fuel surcharge (BAF) quarterly. The July 1 update will reflect the sharply higher fuel prices of recent months — it is expected to be a significant jump. This is one of the main reasons shippers are rushing to move cargo in June.

One piece of good news: diesel prices dropped about 10 cents per liter in the Netherlands this week, on news of a possible ceasefire between the US and Iran. If a deal is reached, fuel costs could ease and lower surcharges would follow in the coming months. (Nieuwsblad Transport)

The UK is introducing a levy on greenhouse gas emissions from ships — similar to what the EU already does. From July 1, carriers will pay a fee based on CO₂ emitted while in UK waters, and will pass this on in your invoice. (UK government website)

If any of your shipments call at UK ports, expect a new cost line on your invoice from July. Carriers like ONE will add this to their existing emissions surcharge (EES). We will keep you updated as carriers confirm their specific rates.

Despite the disruption in the Middle East, global air freight volumes grew 4% in April compared to a year earlier, according to IATA. The growth is mainly on routes from East Asia, where demand remains strong.

The winners and losers of the current situation:

Kerosene (jet fuel) costs were up 121% year-on-year in April. Airlines are passing these costs on through fuel surcharges, and air freight rates are expected to increase in the coming months as a result.

If you use air freight for time-sensitive cargo, factor in higher fuel surcharges over the coming months. The situation in the Middle East is the main driver — if tensions ease, costs could stabilize. We will keep you updated.