Cooling spot rates, air freight volatility & Hormuz rerouting

Team Shypple

April 20, 2026

Welcome back.

Shypple Port Tour Event, Rotterdam 16 apr

Together with a group of 80 of our customers and Shypple colleagues, we hosted a highly successful deep dive into the heart of our industry. We took a boat tour through the Port of Rotterdam, followed by an exclusive tour and a presentation directly at the terminal. Even for industry veterans who have worked in supply chain for years, seeing the sheer scale of these operations and the daily physical workings of the port's daily physical operations up close remains an inspiring experience.

Please note: The geopolitical situation in the Middle East is very dynamic. The information below reflects the current status, but the news is developing quickly and the situation on the water may shift again in the coming days.

What is happening in the Strait:

Strait re-closed: After a brief reopening on Friday, Iran has once again closed the Strait of Hormuz to commercial shipping. Tehran stated this is a direct response to the ongoing US blockade of Iranian ports. (Nieuwsblad Transport)

Escalations on the water: Tensions are high. Maritime authorities report that at least two merchant vessels attempting to pass the Strait were fired upon without warning by the Iranian Revolutionary Guard. (Nieuwsblad Transport)

Patchwork routing: Ocean carriers have been forced into rapid operational changes. After an initial halt, trade is flowing again via indirect, multimodal routes and alternative hubs outside the immediate danger zone. While trade "finds a way," these diversions come with significantly longer transit times and much higher costs.

Fuel squeeze: With the Gulf functioning as a no-go zone, carriers are shifting their refuelling (bunkering) to alternative locations like Singapore. This sudden shift is causing local supply squeezes and driving up global bunker prices.

The long-term impact on the supply chain According to maritime analysts at Drewry, this crisis could permanently reshape global shipping networks. The industry is currently shifting from "cost-optimized" supply chains to "risk-managed and resilience-focused" networks. To reduce exposure to future disruptions, carriers are increasingly redesigning their routes to reduce dependency on major maritime choke points like the Strait of Hormuz or the Suez Canal. For importers and exporters, this means that longer transit times and higher baseline costs may become a permanent feature of global trade. (The Loadstar)

Ocean rates: market cools down as demand softens

After weeks of volatility driven by the Middle East conflict, container spot rates are declining for the first time in six weeks. Market data confirms that the recent rate surges were primarily fueled by emergency bunker surcharges, not by an increase in actual cargo demand.

What is happening in the market:

Falling spot rates: To protect their volumes and keep vessels full, almost all carriers are now actively offering discounts on FAK (Freight All Kinds) and spot rates. For example, the Shanghai-Rotterdam benchmark dropped by 3% this week.

Soft demand: Unlike the pandemic-era, current European demand for Asian goods is noticeably weak. Many retailers are slowing down production and adopting a 'wait-and- see' approach regarding the geopolitical situation.

Stable capacity: Structural vessel capacity on the Asia-Europe trade has actually grown. Currently, there are no reported issues with acquiring vessel space or empty equipment in Asia.

Blank sailings to defend price floors: To prevent base rates from sliding back to absolute minimums, carriers are preparing 'blank sailing' programs. These are designed to temporarily tighten capacity and support planned Peak Season Surcharges (PSS), expected to take effect around early May. (The Loadstar)

Trucking: Italian strike may disrupt supply chains

A planned nationwide strike by Italian road transport operators could disrupt cross-border and intermodal freight flows across Europe this month.

Nationwide strike (April 20 - 25): Italian haulage groups, led by industry associations Trasportounito and Unatras, have called for a major stoppage of road transport services to protest the surging costs of diesel.

Widespread protests: The action will be supported by approximately 100 coordinated protests and roadblocks across Italian cities and towns.

Severe port disruptions: The movement of containers to and from Italian ports is expected to face severe bottlenecks.

Intermodal impact: Because a large share of freight to and from Italy relies on intermodal transport, the road blockages will likely create ripple effects, delays, and backlogs across broader European supply chains. (The Loadstar)

What to expect for your current shipments: If your cargo is currently in transit in Italy or ready for pickup between April 20 and 25, expect immediate delays. Shipments already at Italian ports or rail terminals are likely stuck until the blockades are lifted. For cargo ready to be loaded, collections will be postponed to the next available departure.

Airfreight: Market far from normalization despite ceasefire

Despite the recent US-Iran ceasefire, analysts warn that the global air freight market will not return to normal anytime soon. The industry has entered a highly volatile phase where capacity constraints, soaring fuel costs, and geopolitical risks have overtaken standard seasonal trends as the primary drivers of pricing.

Delayed recovery and fuel spikes: A ceasefire does not immediately restore normal supply chain conditions. Jet fuel prices have risen sharply, and rebalancing fuel supply chains may take months.

Rates driven by tight supply, not demand: Spot rates are surging globally. The Baltic Air Freight Index rose over 25% recently, and rates from India to Europe have more than doubled. This spike is driven by cost inflation and restricted supply, rather than a rise in consumer demand.

Network reconfiguration: Airlines are redrawing their global networks to avoid Middle Eastern choke points. Cargo is being pushed through alternative, more direct corridors or secondary hubs. While trade continues, it comes with less flexibility, longer transit times, and much higher operational costs.

Fragmented capacity: Although global freighter capacity has not collapsed, effective capacity remains tight due to the longer routings and operational inefficiencies. (The Loadstar)

What to expect for your current shipments: If your air freight is currently in transit or ready to fly, expect it to take longer than standard schedules indicate. Due to sudden rerouting around the Middle East, flight times have increased and alternative hubs are experiencing congestion. Additionally, be prepared for high and fluctuating fuel surcharges on your final invoice. If your cargo is ready but not yet booked, anticipate limited immediate space and significantly higher spot rates compared to last month.

Europe Faces Imminent Jet Fuel Shortages

The ongoing disruption in the Middle East is moving beyond freight rate increases and is now directly threatening the physical supply of jet fuel across Europe.

What is happening:

High dependency: The Middle East typically supplies up to 75% of Europe's jet fuel imports. The current stalemate around the Strait of Hormuz is severely restricting these critical oil flows.

Dropping inventories: Fuel reserves at major European hubs, including the Amsterdam-Rotterdam-Antwerp (ARA) region, have rapidly dropped to the bottom of their five-year averages.

Looming flight cancellations: The International Air Transport Association (IATA) and the International Energy Agency (IEA) warn that a "systemic" shortage could emerge soon. If European fuel stocks fall below 23 days' worth of supply, authorities will be forced to trigger flight cancellations. Without sufficient alternative supply lines, this critical threshold could be breached as early as late May or June.

💡 What it means for your supply chain: The threat of physical fuel shortages adds a massive layer of risk to air freight for the upcoming summer months. If fuel rationing or flight cancellations are implemented in Europe, available air cargo capacity will plummet, leading to severe backlogs and further rate spikes. We strongly advise mapping out contingency plans immediately.

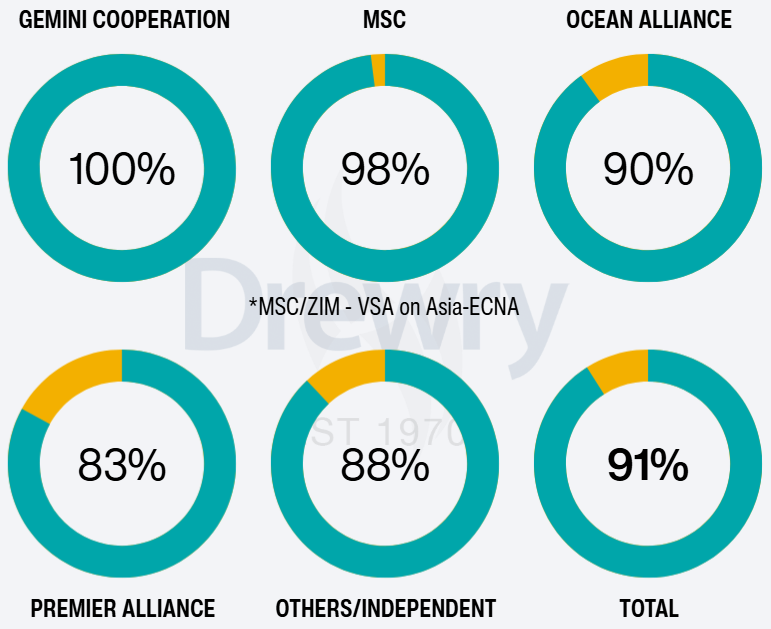

Blank sailings: 9% cancellation rate

From 20 April to 24 May, 9% of sailings have been withdrawn (59 of 685 sailings).

Much will depend on how the situation around the Strait of Hormuz evolves, particularly in terms of security conditions and energy markets.

Most cancellations are concentrated on:

Asia-America routes (54%, was 41%),

followed by Asia-Europe/Med (32%, was 43%),

and finally Europe-America (14%, was 16%).

Yellow represents the percentage of cancelled sailings per carrier alliance. (Drewry)

📌 Port congestion

Rotterdam

Average delay ~ 3 days.

Antwerpen

Average delay ~ 3 days.

Germany ports

Hamburg: average delay ~ 3 days.

Bremerhaven: average delay ~ 1 day.

Top reads from last week:

War in Iran has expedited development of a new trade route, the Gulf land bridge