Welcome back.

As the Chinese New Year holidays wrap up, operations in China are still slowly getting back up to speed. Our internal data shows that a significant number of containers were left behind before the break, which is currently restricting the available space for new bookings. Due to this tighter capacity, we anticipate a slight upward pressure on rates in the short term, although exact market indications have not yet been fully established.

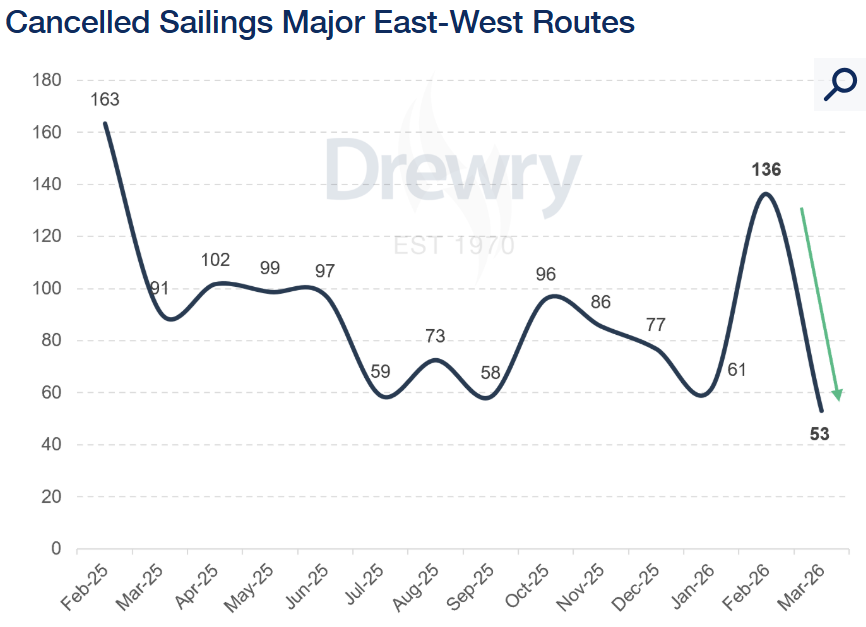

The carrier response: Massive February cuts

To manage the traditional seasonal drop in cargo during the holidays, carriers have aggressively reduced their active capacity. Across the major trades, including Asia-Europe, 136 scheduled sailings were cancelled for February. This represents a massive 122% increase in blank sailings compared to January. Looking ahead to March, the strategy shifts. Currently, only 53 blank sailings have been announced, which will translate to an effective capacity increase of 20% for the month.

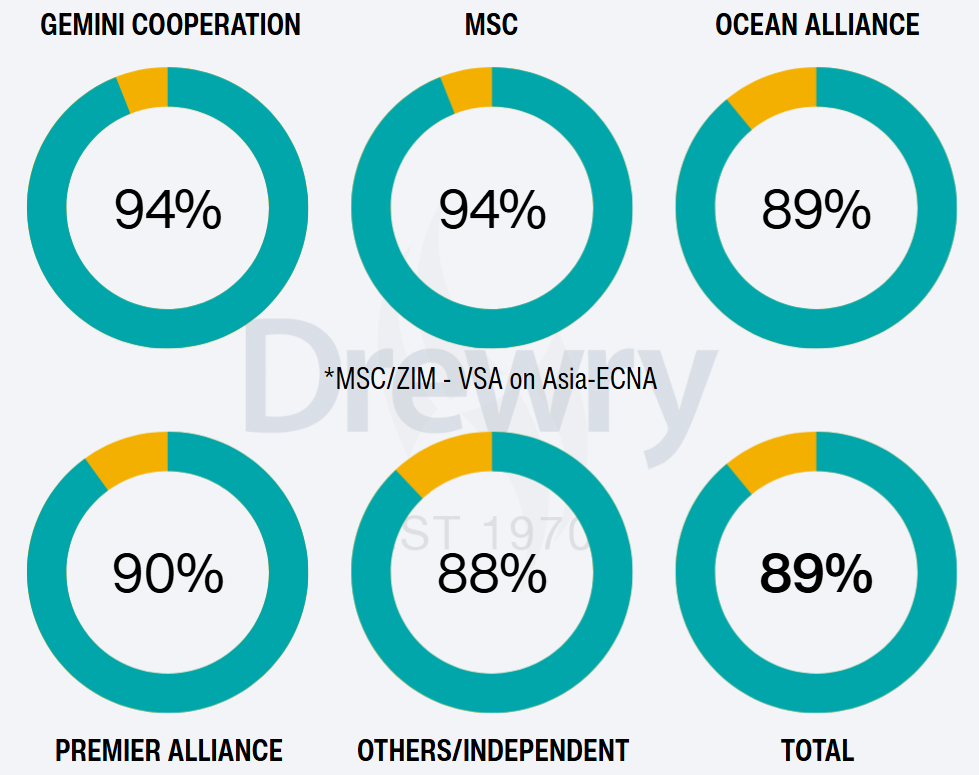

However, carriers are facing a much larger approaching challenge: structural overcapacity. With the global newbuild orderbook currently sitting at 34% of the existing fleet, overcapacity is projected to grow throughout this year and peak around 2027. Analysts predict this surplus could reach levels similar to 2016, a year infamous for intense carrier price wars. How the market balances this will depend heavily on relieving factors like vessel scrapping and the eventual resolution of the Red Sea crisis. (The Loadstar)

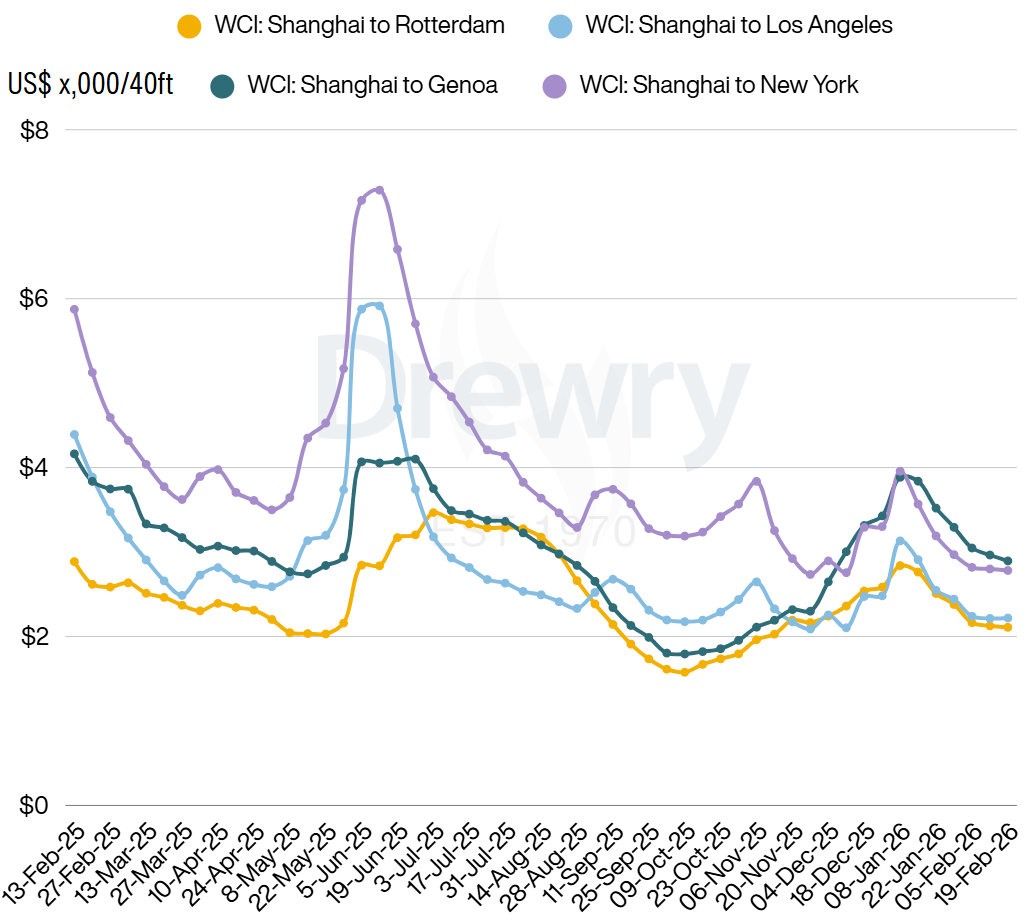

Leading up to the Chinese New Year, container spot freight rates experienced an unusual decline, indicating a weaker-than-expected market. Now that the holidays are concluding, this softening trend is expected to carry on.

Unlike normal seasonal trends, the traditional pre-Chinese New Year airfreight rush did not appear this year. Data shows that global rates remained completely flat compared to the same period in previous years, despite the changing holiday dates.

Demand ahead of the holidays was noticeably less than expected. At the same time, available flight capacity has been restored faster than demand has recovered.

As Chinese factories begin to reopen in early March, a slight recovery in volumes is expected. However, because freighter capacity remains large, the overall market outlook for the coming months points toward continued stability rather than seasonal pricing stress. (The Loadstar)

Final 2025 figures from the Airports Council International (ACI) show a shifting landscape in the European air cargo market. While the average European airport saw a volume growth of 3.2% last year, Schiphol struggled significantly.

Shipping traffic through the icy waters of the Arctic Polar Code area has reached an all-time high. Last year, a record 1,812 unique ships navigated the region, marking a 40% increase compared to 2013. While the Arctic passage is still heavily dominated by fishing vessels, gas tankers, and bulk carriers, container shipping is slowly testing the waters. Only 19 unique container ships made the crossing last year. However, Chinese carrier Sea Legend recently completed an Arctic voyage to Rotterdam and is reportedly considering launching a regular service.

Industry resistance & geopolitics

Despite the potential for shorter transit times between Asia and Europe, mainstream adoption by major carriers remains highly unlikely in the near future.