Middle East crisis, emergency surcharges & new Skal levies

Team Shypple

March 23, 2026

Welcome back.

New Skal levy impacts organic importers

As of April 1, 2026, the landscape for importers of organic products will change significantly. The costs for import inspections from outside the EU (conducted by Skal Biocontrole) will no longer be subsidized by the government. Instead, they will be billed directly to the importer.

Costs per document: Importers will soon pay a fixed fee per checked Certificate of Inspection (COI), with heavy surcharges (up to 100%) applied to inspections taking place outside office hours or during the weekend.

Margin impact: This levy directly impacts the total import costs, especially for businesses that frequently ship smaller loads (LCL) or handle a wide, diverse product range.

Our advice: It is crucial to consolidate shipments and COIs more efficiently if you ship organic goods. Furthermore, ensuring 100% accurate documentation in TRACES before the vessel arrives is now even more important. Administrative errors will immediately result in extra inspection fees and terminal demurrage.

Middle East: Impact on the global supply chain

The ongoing blockade of the Strait of Hormuz has triggered a chain reaction across global logistics. While the worst-case scenarios for ocean freight rates have not yet fully materialized, the operational and economic consequences are getting visible.

Ocean freight rates & surcharges:

Spot market remains stable: Surprisingly, the anticipated explosion of spot rates on the Asia-Europe trade lane has not happened yet. The market is currently rejecting the extreme base rate hikes proposed by carriers.

Surcharges are skyrocketing: To compensate for this, carriers are drastically increasing their Emergency Fuel Surcharges (EFS). We are seeing these surcharges nearly double within a very short period of time. (Nieuwsblad Transport)

Operational chaos: 200,000 containers stuck

Trapped capacity: An estimated 3,200 ships with around 20,000 seamen and 200,000 containers are currently stuck in and around the Persian Gulf. The IMO (International Maritime Organization) is urgently pushing for a safe maritime corridor to free these vessels.

Alternative routing: Ships that are unable to enter the Gulf are forced to discharge their cargo in ports like India or Pakistan, meaning the freight has to be rerouted via alternative, slower paths to reach its final destination. (Nieuwsblad Transport)

Impact on European importers and exporters: This impacts the European energy-intensive industries. Logistics managers should prepare for this ongoing energy crisis to translate into higher overall supply chain costs and rising inflation in the coming months. (Flows)

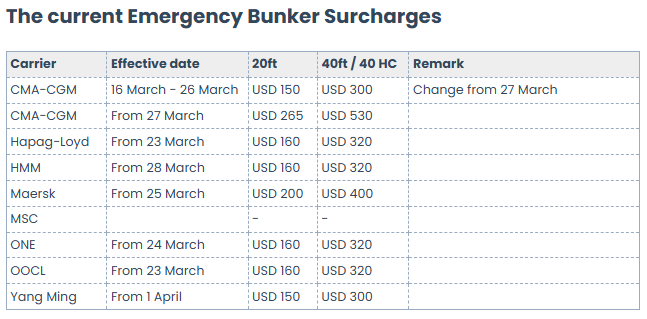

Due to the rapidly escalating situation in the Middle East and the closure of the Strait of Hormuz, the global container market is facing severe instability. Global fuel prices have surged dramatically since the beginning of the month, and ocean carriers are now passing these skyrocketing bunker costs directly on to the market.

What this means for your shipments: To maintain their services, carriers have announced the immediate implementation of an Emergency Fuel Surcharge (EFS), also referred to as an Emergency Bunker Surcharge (EBS).

Global impact: This surcharge is not limited to shipments routed through the Middle East; it is currently affecting almost all major global trade lanes for both imports and exports. Besides that it is not only for new bookings but also for shipments that are already booked.

Not always allowed: In some cases this is not allowed as there is a SSE Filing registration required in China. In this case, it will be included as part of the ocean freight, so no SSE filing registration is required.

Continuous fluctuations: Because global fuel markets remain highly volatile, carriers are constantly adjusting these surcharges at very short notice. Every adjustment will be weekly updated in our Emergency Bunker Surcharges page

Air freight: Flight suspensions and imminent fuel shortages

The ongoing conflict in the Middle East is increasingly disrupting global air freight operations. What started as airspace safety restrictions is now evolving into significant capacity and fuel supply challenges, particularly affecting routes connecting Europe, the Middle East, and Asia.

Key developments impacting your air freight:

Crucial hubs bypassed: KLM has extended the suspension of all flights to major Middle Eastern transit hubs, including Dubai, Riyadh, and Dammam, until May 17th. As the Middle East normally serves as a vital transit point for global air cargo, these ongoing cancellations significantly reduce available capacity. (Nieuwsblad Transport)

Fuel shortages in Southeast Asia: The blockade of fuel exports from the Gulf region is impacting Southeast Asian countries. Carriers like Air France-KLM are actively preparing for scenarios where return flights from Asia might face severe fuel shortages. This could force airlines and regional airports to limit their flight schedules in the near future.

Skyrocketing kerosene prices: With jet fuel prices more than doubling compared to last month, airlines are facing massive operational costs. Consequently, carriers are rapidly introducing or increasing fuel surcharges across the board to offset these spikes. (Nieuwsblad Transport)

High diesel prices force operational changes

The record-high diesel prices are currently causing challenges within the European trucking transport sector, leading to instant operational adjustments on the road.

Lower speeds to save fuel: To mitigate the extreme fuel costs, trucking companies are structurally adjusting their driving behavior. Carriers are lowering the maximum speed of their vehicles, optimizing tire pressure, and adopting more fuel-efficient driving habits.

Delayed cost processing: While roughly 80% of carriers have clauses to pass these increased fuel costs on to their clients, the delay in invoicing is causing short-term cash flow issues for many transport companies. (Nieuwsblad Transport)

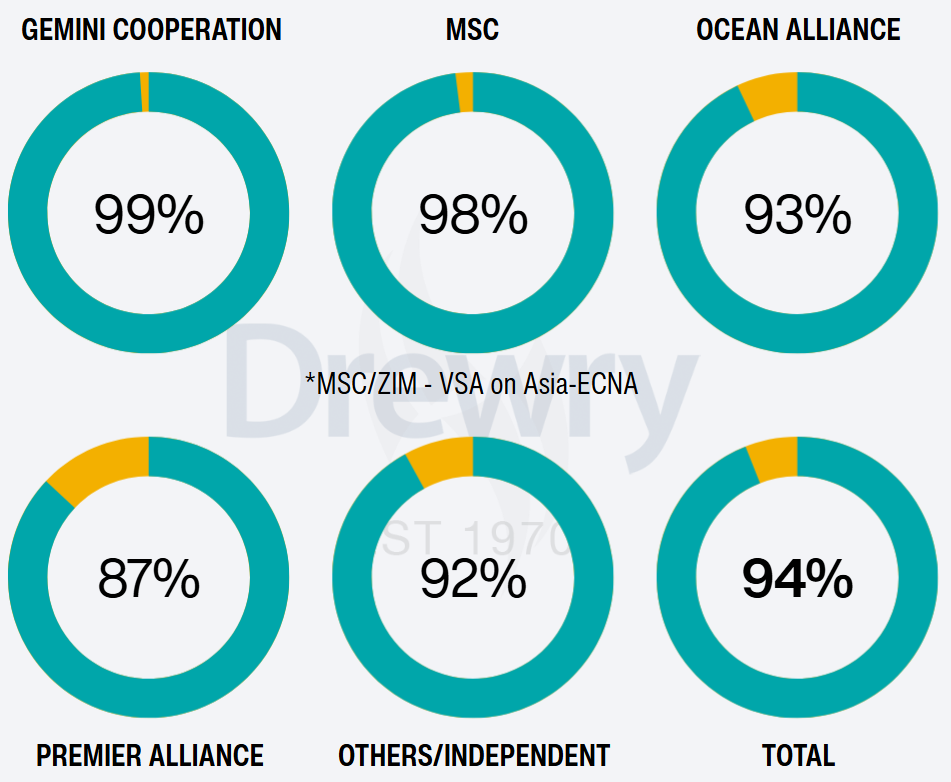

Blank sailings: 6% cancellation rate

From 23 March to 26 April, 6% of sailings have been withdrawn (43 of 708 sailings).

Holding steady, but under pressure. Global container markets are adapting to the Strait of Hormuz disruptions. Operational impacts remain limited, with carriers adjusting networks while maintaining service continuity across key routes.

Most cancellations are concentrated on:

Asia-America routes (58%, was 53%),

followed by Asia-Europe/Med (28%, was 20%),

and finally Europe-America (14%, was 27%).

Yellow represents the percentage of cancelled sailings per carrier alliance. (Drewry)