10% of global traffic experience disruptions, rising surcharges & airfreight capacity grounded

Team Shypple

March 9, 2026

Welcome back.

Global supply chain disrupted by Hormuz closure

The escalating crisis in the Middle East is causing massive disruptions across the global logistics chain. Following threats from the Iranian Revolutionary Guard to set fire to any vessel attempting to pass, the Strait of Hormuz is effectively blocked.

The bottleneck in the Persian Gulf

Approximately 3,200 ships are currently stuck in the Persian Gulf, representing about 4% of total global shipping tonnage.

This includes 112 oil tankers and 132 container ships holding roughly 458,000 TEU. However, broader estimates indicate that more than 2 million TEU are currently stuck in the wider region.

Safe departure from the Gulf is now virtually impossible, as maritime insurers are no longer covering these high-risk voyages.

Carrier responses

Several carriers have announced booking stops for the Middle East. MSC has taken the most drastic step, halting all container bookings for the entire region, while others are pausing specific cargo like reefers and dangerous goods.

While Persian Gulf ports normally account for 3.3% of global container throughput, analysts warn that up to 10% of global container traffic will experience disruptions due to interconnected international supply chains. Trapped vessels and containers miss their usual loops in Asia and Europe, causing sudden capacity and equipment shortages worldwide.

Capacity is being actively shifted to other trades. For other origins, including China and the Far East, carriers are responding with direct rate increases and additional surcharges. (Nieuwsblad Transport)

Global impact

The global market is feeling the strain: the conflict is driving up fuel prices, insurance premiums, and freight rates. Notably, one-tenth of the oil normally transiting to the Port of Rotterdam passes through the Strait of Hormuz, severely disrupting the global oil and gas market.

Impact export

While the direct impact on total container exports seems limited, companies that export heavily to the Middle East are facing severe damages.(Nieuwsblad Transport)

The financial impact is hitting all export trades. Carriers are now applying an Emergency Fuel Surcharge (EFS), also known as an Emergency Bunker Surcharge (EBS), to all export shipments, adding anywhere from €80 to €150 per TEU.

Middle East conflict drives up rates

The escalation in the Middle East is leading to rapid increases in freight rates and operational costs. Analysts expect a sharp upward correction in rates in the coming weeks. This will be driven by both the Middle East crisis and Asian factories resuming normal production volumes after the Chinese New Year.

We anticipate the market to remain highly unstable in the coming months. The massive rerouting of vessels is throwing the supply chain out of balance, which will likely lead to:

Container equipment ending up in the wrong locations.

Severe depot congestion and extended transit times.

Carriers attempting to reopen or renegotiate existing rate agreements.

Immediate rate spikes & surcharges

Surging spot rates: Data shows a 9% rate increase on the Asia - Europe route compared to the days just before the attacks began. Closer to the conflict zone, rates from China have surged by 28% to Salalah (Oman) and 17% to Colombo (Sri Lanka), respectively.

New surcharges: Carriers are actively rolling out direct rate increases and new fees for origins like China and the Far East. We are now seeing Emergency Fuel Surcharges (EFS), War Risk/Security fees, and various other operational surcharges. Even European shortsea operators are introducing 'Cost Recovery Charges' to offset the immediate spike in their network costs.

Fuel prices & insurance pressures

The blockade of the Strait of Hormuz, a route that handles approximately 20% of the world's oil supply, is pushing up global prices due to supply concerns. This leads to higher bunker fuel costs for carriers, driving up total freight expenses.

While maritime insurance for Hormuz transits is still technically available, it has become significantly more expensive and scarce. (Nieuwsblad Transport)

Airfreight: Middle East conflict grounds 20% of global capacity

Air cargo is piling up at major European airports, including Schiphol. The Gulf region is a crucial global transit corridor between Europe and Asia, and the current airspace closures are severely disrupting global trade.

Grounded fleets & closed hubs

Nearly 20% of global airfreight capacity is currently grounded.

The airspace around key hubs like Doha, Dubai, and Abu Dhabi is closed due to drone and missile attacks.

Qatar Airways Cargo and Emirates SkyCargo have grounded their fleets and are holding accepted cargo at global stations.

FedEx has completely halted flights and depot intake for 11 countries in the Middle East.

Meanwhile, airlines like KLM and Cathay Group are canceling flights or avoiding the airspace entirely, though UPS continues to operate by utilizing alternative routes.

Rerouting flights requires more fuel and reduces the cargo payload per flight. Combined with spiking kerosene prices and rising insurance premiums, analysts expect steep price increases across the board. Freightos warns that transit cargo currently stuck between Europe and Asia will face significant delays. Even when the airspace reopens, history shows it could take weeks for airlines to clear the backlogs. (Nieuwsblad Transport)

Forwarders are proactively pulling booked freight from airlines back to their own warehouses. They are urgently searching for alternative transit hubs to bypass the Middle East. Relying on their pandemic experience, forwarders are securing direct flights with minimal layovers to keep supply chains moving. . (Nieuwsblad Transport)

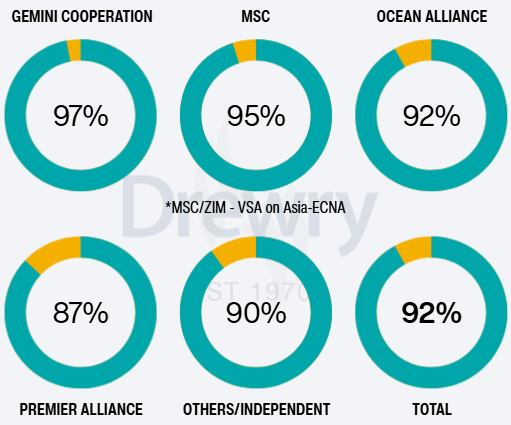

Blank sailings: 8% cancellation rate

From 9 March to 12 April, 8% of sailings have been withdrawn (55 of 705 sailings).

This number has decreased again. Port congestion, ongoing rerouting and operational adjustments could gradually tighten effective capacity if vessels and empty equipment remain tied up on longer rotations.

Most cancellations are concentrated on:

Asia-America routes (53%, was 61%) ,

followed by Europe-America (27%, was 16%)

and finally Asia-Europe/Med (20%, was 24%).

Yellow represents the percentage of cancelled sailings per carrier alliance. (Drewry)

Port of Rotterdam's 2025 results

While the Port of Rotterdam saw a slight overall increase in container traffic in 2025, the underlying cargo flows are sending a warning signal about the European economy.

Last year, the port recorded a 4% increase in the import of containers, but a 4% decline in the export of containers. As a result, Rotterdam is exporting significantly more empty containers back abroad. The neighboring Port of Antwerp reported a very similar shift toward a larger import share in its 2025 figures.

The Port of Rotterdam warns that shipping empty containers instead of manufactured goods is a concerning trend. Consuming high volumes of imports while producing less threatens to hollow out the European economy and job market.

The drop in export goods (such as machinery, chemicals, and vehicles) highlights the declining competitive position of European industries. This downturn is visible across multiple sectors, including a noticeable drop in raw materials destined for German steel production.

Looking ahead The investment climate in Europe remains under heavy pressure, evidenced by several factory closures and canceled projects in 2025, despite Rotterdam's excellent logistical location and hinterland connections. To reverse this trend and retain local manufacturing, the Port of Rotterdam is urging the government to improve the business climate by avoiding strict national regulations that go beyond existing European rules. (Nieuwsblad Transport)